![]()

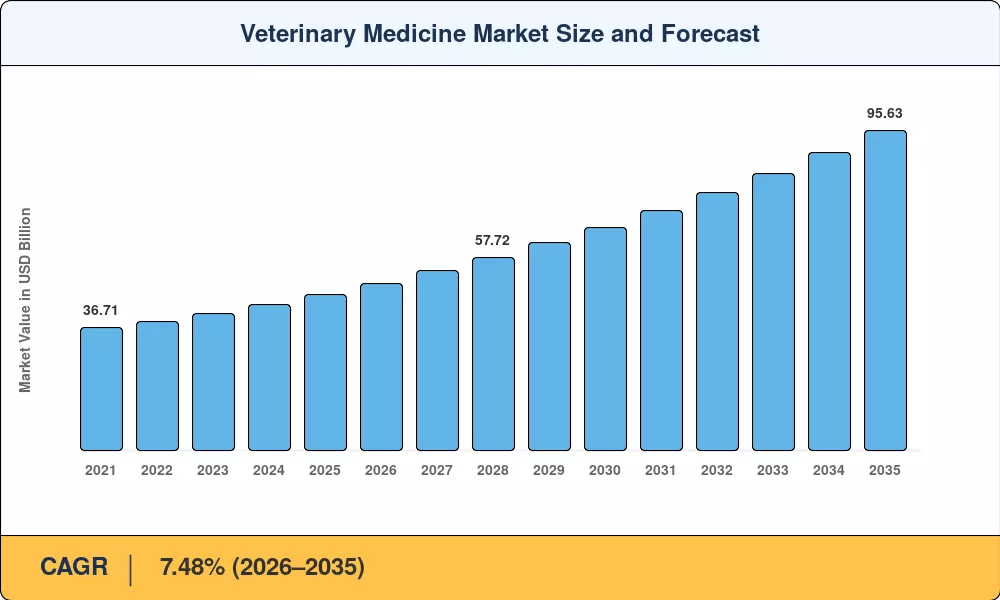

Veterinary Medicine Market to Surge from USD 49.96 Billion in 2026 to USD 95.63 Billion by 2035-By Rising Pet Humanization, Antibiotic Stewardship Mandates

NY, CA, UNITED STATES, June 18, 2026 /EINPresswire.com/ — As per Market Research Future, the global Veterinary Medicine Market size to reach USD 95.63 Billion by 2035 from USD 49.96 Billion in 2026, at a CAGR of 7.48% during the forecast period 2026–2035. The market base was estimated at USD 46.48 Billion in 2025.

The 7.48% CAGR—anchored by structural demand for animal health rather than discretionary spending—is driven by three converging forces: rising global pet ownership and humanization that continues to widen the addressable patient base for companion animal pharmaceuticals, sustained antibiotic stewardship regulation that has redirected livestock veterinary care from therapeutic antibiotics to preventive vaccines and biologics, and biologics platform expansion that has pulled veterinary medicine from commodity generics into high-margin monoclonal antibody and recombinant vaccine portfolios.

National governments and multilateral health organizations are amplifying this momentum. The American Pet Products Association reports that 67% of U.S. households—approximately 87 million homes—owned a pet in 2024, up from 56% a decade earlier. Because average annual per-pet pharmaceutical expenditure now surpasses USD 400 in the United States, this demographic wave mechanically expands the addressable population for pet health medications and chronic-disease management.

The EU’s Regulation 2019/6 and the FDA’s five-year antimicrobial resistance action plan have collectively removed over 70 previously approved antibiotic feed-grade indications since 2022, redirecting demand toward vaccines and probiotics.

Venture capital deployed into companion animal pharmaceuticals exceeded USD 2.8 billion globally in 2024, reflecting investor conviction that biologics—which carry gross margins of 40–60% versus 20–30% for generics—will anchor the next innovation cycle. Together, these initiatives are creating the procurement infrastructure and delivery innovation on which the Veterinary Medicine Market depends.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/844

Key Market Trends & Growth Drivers

Rising Pet Ownership and Humanization

The American Pet Products Association reported that 67% of U.S. households—approximately 87 million homes—owned a pet in 2024, up from 56% a decade earlier. This structural shift is translating pet health medications from a discretionary spend into a recurring healthcare obligation, with average annual per-pet pharmaceutical expenditure surpassing USD 400 in the United States. Asia-Pacific mirrors this trajectory: China’s urban pet population exceeded 120 million in 2024, creating an addressable companion animal pharmaceuticals pool worth over USD 5.2 billion.

National pet registries in India and South Korea are also capturing higher adoption rates as urbanization accelerates, feeding into the Veterinary Medicine Market growth pipeline across emerging economies. Each percentage point of pet ownership gain translates into measurable prescription volume for companion animal pharmaceuticals, and the chronic-disease management schedule embedded in routine veterinary care makes this driver structurally durable through 2035.

Extended survival in companion animals—driven by advances in oncology, cardiology, and endocrinology extending median life expectancy—creates a larger prevalent population requiring sustained pet health medications. Longer lifespans transform pet ownership from an acute-care relationship into a chronic-disease management paradigm with sustained pharmaceutical utilization.

Early-adopter veterinary health systems report that AI-enhanced diagnostic platforms detect subclinical disease at earlier stages, converting patients who would previously have presented with advanced illness into candidates for preventive pharmacotherapy. Machine-learning algorithms trained on over 2 million veterinary imaging datasets now detect metabolic and neoplastic conditions 12–18 months earlier than conventional screening protocols.

Antibiotic Stewardship and Regulatory Mandates

The EU’s Regulation 2019/6 and the FDA’s five-year antimicrobial resistance action plan have collectively removed over 70 previously approved antibiotic feed-grade indications since 2022, redirecting demand toward vaccines and probiotics. The Veterinary Medicine Market benefits directly as producers substitute growth-promoting antibiotics with licensed immunological alternatives, elevating vaccine revenue share across both poultry and swine segments.

The EU’s Farm to Fork strategy targets a 50% reduction in antimicrobial sales for food-producing animals by 2030, creating the single largest catalyst converting antibiotic prescriptions to vaccine-based animal disease treatment regimens across the continent.

Pooled procurement through national health and agricultural systems drives per-dose prices down for high-volume livestock vaccines, expanding access while compressing manufacturer margins. The convergence of diagnostic platforms with preventive vaccination programs is creating integrated animal health management systems that personalize livestock veterinary care at scale.

Zoetis committed significant R&D investment toward recombinant and mRNA vaccine platforms from 2022 to 2025. By 2030, an estimated 40% of newly enrolled commercial poultry operations will undergo diagnostic screening followed by matched vaccination protocols, creating a diagnostic-therapeutic revenue loop. In the US, vaccine adoption is accelerating as integrated livestock operations build biosecurity-grade infrastructure.

Biologics and Recombinant Platform Expansion

Legacy small-molecule generics, long the default therapeutic modality, are giving ground to recombinant platforms, monoclonal antibody therapies, and gene-edited vaccines. Pet owners are willing to pay more for innovative biologic medicines, as demonstrated by the success of products like Librela (for osteoarthritis pain in dogs) and Solensia (for cats).

The veterinary industry is moving toward high-value, recurrent customized treatments as a result of these medications, which offer efficient, targeted care in favor of more conventional anti-inflammatories. The U.S. Department of Agriculture committed to streamlined approval pathways for novel veterinary biologics, directly addressing regulatory bottlenecks that have constrained advanced animal disease treatment adoption.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/844

Market Segment Insights

BY PRODUCT TYPE

Drugs: Dominant segment with ~52.5% revenue share in 2025. Reflecting entrenched physician familiarity with broad-spectrum anti-infectives and parasiticides. Parasiticide revenues alone accounted for over USD 8 billion globally in 2025, with isoxazoline-class products dominating companion animal pharmaceuticals and driving repeat-purchase economics. Hospital and clinic procurement teams treat them as default first-line agents, and generic pricing has enabled broad adoption even in cost-sensitive emerging markets.

Vaccines: Fastest-growing product segment at 9.70% CAGR (2026–2035). Driven by recombinant and mRNA platform adoption and expanding livestock veterinary care indications. Zoetis’s mRNA vaccine pipeline generated significant 2024 revenue, and pipeline candidates targeting avian influenza, foot-and-mouth disease, and African swine fever could double the segment’s addressable population by 2030. The convergence of diagnostic platforms with matched therapeutic vaccines is creating integrated animal health management systems that personalize livestock veterinary care at scale.

Medicated Feed Additives: USD 7.88 Billion in 2025. Antibiotic-alternative supplementation maintains strong formulary positioning as producers transition from growth-promoting antibiotics to licensed immunological and nutritional alternatives. Biosimilar and generic candidates from Phibro and others are advancing through regulatory review, projected to trigger 20–30% price erosion within three years of launch.

BY ANIMAL TYPE

Companion Animals: Dominant animal type with ~51.5% revenue share in 2025. Approximately 67% of U.S. households now own pets, making companion animal pharmaceuticals a near-universal component of the pet care pathway. The inherent premiumization of pet health—driven by humanization trends and insurance penetration—drives sustained dual-channel demand for preventive and therapeutic pet health medications.

Livestock Animals: Fastest-growing animal type segment at 11.24% CAGR (2026–2035). Reflecting industrialized livestock production that extends the window for animal disease treatment. Antibiotic stewardship regulations and export compliance requirements create a larger prevalent population requiring sustained livestock veterinary care, particularly across poultry and swine biosecurity protocols.

BY ROUTE OF ADMINISTRATION

Parenteral: Dominant route with ~44.0% revenue share in 2025. Hospital and clinic injection infrastructure dominates volume, channeling routine vaccine and biologic supply. Injectable vaccines and monoclonal antibodies delivered in veterinary hospital settings anchor this segment.

Oral: USD 14.20 Billion in 2025. Patient preference and home administration sustain demand for oral parasiticides and supplements, particularly chewable formulations for companion animals.

BY END USER

Veterinary Hospitals: Largest segment with ~53.5% share in 2025. Comprehensive veterinary service lines and complex diagnostic and surgical cases dominate volume. Hospitals remain the primary delivery site for advanced animal disease treatment with biologics due to specialized equipment, reference laboratory access, and pharmaceutical dispensing requirements.

Veterinary Clinics: Fastest-growing end-user segment at 11.65% CAGR (2026–2035). Outpatient shift and telehealth-routed prescriptions drive demand as connected diagnostic platforms reduce the need for centralized hospital visits. Community clinics increasingly prescribe chronic-care pet health medications and routine livestock vaccinations to manage hospital capacity.

Read Detailed Insights:

https://www.marketresearchfuture.com/reports/veterinary-medicine-market-844

Regional Outlook

North America — Dominant Market (~38.1% Share, 2025)

The United States generates approximately 82.4% of North American Veterinary Medicine Market revenue, driven by the USD 36+ Billion companion-animal care economy, pet insurance penetration now above 4.6%, and broad reimbursement for advanced pet health medications—a single policy ecosystem that converted a discretionary spend into a structural preventive care tail.

USDA streamlined approval pathways for novel veterinary biologics have driven adoption in academic and corporate veterinary centers, while community clinics increasingly prescribe chronic-care pet health medications to manage hospital capacity. The US dominates through a combination of high per-pet spending, robust payer coverage, and rapid biologic adoption.

Europe — Second Largest (~27.0% Share, 2025)

Europe’s Veterinary Medicine Market reflects divergent national strategies—Germany leads regionally with advanced diagnostics and companion animal spending, contributing 22.8% of regional share, while the UK historically used selective pet insurance targeting before broadening coverage through technology appraisals for biologics at 8.92% CAGR.

France contributes significantly through large-animal vaccine programs at USD 1.85 Billion in 2025. Italy contributes on aquaculture therapeutics at 8.30% CAGR. Spain is growing steadily on swine biologics demand at USD 1.24 Billion in 2025.

Asia-Pacific — Fastest-Growing Region (10.80% CAGR, 2026–2035)

Asia-Pacific is the engine of the Veterinary Medicine Market. China holds the largest regional share with ~34.6% of regional revenue, driven by rapid pet adoption with urban pet population exceeding 120 million in 2024 and swine vaccination programs—instantly creating an addressable companion animal pharmaceuticals pool worth over USD 5.2 billion.

India is growing at 12.15% CAGR on the back of National Livestock Mission investment exceeding USD 800 million toward animal health infrastructure. Japan contributes USD 2.18 Billion through premium companion animal pharmaceuticals at steady pace. South Korea is growing at 11.48% CAGR on pet humanization trend.

Middle East & Africa — Emerging Opportunity (USD 2.60 Billion, 2025)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with National Transformation Program targeting 80% poultry self-sufficiency by 2030, contributing ~28.5% of regional share—NEOM health cluster and the UAE’s Cleveland Clinic and Mayo Clinic affiliations have created pockets of excellence for advanced animal disease treatment.

South America — Growing Presence (USD 3.16 Billion, 2025)

Brazil anchors South America’s Veterinary Medicine Market at ~58.3% of regional revenue, with the world’s largest poultry exporter status mandating rigorous vaccination and animal disease treatment compliance to meet sanitary standards from the EU, Japan, and Middle Eastern importers, providing a stable demand floor that smooths regional forecasts. Access to advanced biologics remains limited by cold-chain infrastructure gaps, though domestic production feasibility studies are underway. Argentina is growing at 9.52% CAGR on cattle vaccination mandates.

Competitive Landscape and Recent Developments

The Veterinary Medicine Market exhibits moderate concentration, with the top four companies collectively holding an estimated 55–60% of global revenue. The Herfindahl-Hirschman Index sits between 1,200 and 1,500, reflecting a moderately consolidated structure where scale advantages in R&D, regulatory dossier breadth, and multispecies portfolios create durable competitive moats.

The competitive landscape is stratified between vertically integrated leaders serving global companion and livestock markets, vaccine portfolio specialists capturing government and corporate tenders, and diagnostic ecosystem developers consolidating the animal clinical diagnosis segment.

KEY COMPANIES AND RECENT MILESTONES

Merck Animal Health (2024–2025): Ruminant vaccines, aqua health, and companion therapeutics reinforce the strong livestock veterinary care footprint positioning, holding ~9–12% of global revenue. Acquired Elitechvet diagnostic assets in June 2023, expanding its reference-laboratory footprint in Europe and strengthening its animal disease treatment portfolio.

Elanco Animal Health (2024–2025): Parasiticides, medicated feed, and pet wellness reinforce the leveraging Bayer Animal Health integration synergies positioning, holding ~7–10% of global revenue. Launched Credelio Quattro, a combination parasiticide covering heartworm, fleas, ticks, and intestinal worms in a single monthly chewable dose for companion animal pharmaceuticals in March 2024. Received FDA approval for Credelio Quattro for cats in December 2025.

IDEXX Laboratories (2024–2025): In-clinic diagnostics, reference lab, and cloud analytics reinforce the diagnostic ecosystem driving Rx pull-through positioning, holding ~4–6% of global revenue. Introduced the Procyte One hematology analyzer with AI-assisted cell classification in September 2023, advancing point-of-care animal clinical diagnosis capabilities globally.

Future Outlook: 2026–2035

By 2030, precision biologics and integrated diagnostic-therapeutic platforms will become the operating system of veterinary medicine management. The convergence of companion animal diagnostics and targeted monoclonal antibody therapy will reshape the Veterinary Medicine Market through the late 2020s. By 2030, an estimated 40% of newly diagnosed chronic conditions in companion animals will undergo diagnostic screening followed by matched biologic therapy, creating a diagnostic-therapeutic revenue loop. The USDA’s streamlined biologics approval pathways ensure domestic vaccine supply scales alongside clinical demand. Machine-learning models that integrate genomic, proteomic, and imaging biomarkers can recommend optimal sequencing of parasiticides, vaccines, and biologics for individual patients. Start-ups have raised over USD 800 million in venture funding for veterinary decision-support tools since 2023.

Biosimilar-driven access expansion and AI-integrated clinical decision support will reframe cost structures by the early 2030s. Patent expirations for key biologics (expected 2025–2027 in key markets) will trigger biosimilar entry that could reduce pet health medication costs by 20–30%. While this compresses per-unit revenue, volume expansion—particularly in Asia-Pacific and South America—is projected to more than offset pricing headwinds. The net effect accelerates Veterinary Medicine Market penetration in markets where out-of-pocket costs currently limit animal disease treatment initiation. AI-integrated clinical decision support platforms will guide optimal sequencing of vaccination and treatment regimens by 2028–2030. Veterinary medical associations are developing clinical-decision-support frameworks that embed AI recommendations into electronic health records, standardizing vaccine initiation criteria across practice settings.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/veterinary-animal-vaccines-market-2687

https://www.marketresearchfuture.com/reports/veterinary-diagnostics-market-21729

https://www.marketresearchfuture.com/reports/animal-health-market-7163

https://www.marketresearchfuture.com/reports/companion-animal-healthcare-market-1168

https://www.marketresearchfuture.com/reports/animal-antibiotics-and-antimicrobials-market-6680

https://www.marketresearchfuture.com/reports/veterinary-imaging-market-2919

https://www.marketresearchfuture.com/reports/veterinary-surgical-instruments-market-2785

https://www.marketresearchfuture.com/reports/pet-insurance-market-12399

https://www.marketresearchfuture.com/reports/veterinary-telehealth-market-42407

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery